“The crisis takes a much longer time coming than you think, and then it happens much faster than you would have thought, and that’s sort of exactly the Mexican story. It took forever and then it took a night.”

– Rudiger Dornbusch

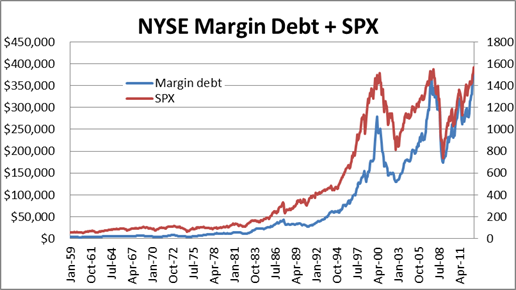

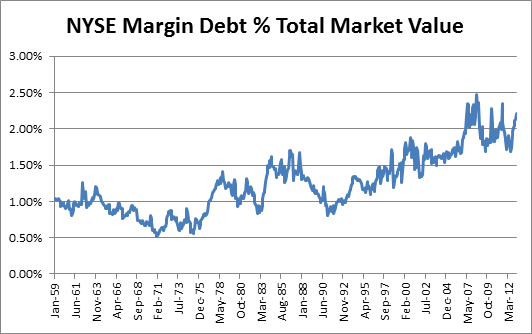

There have been some articles circulating about NYSE margin debt, e.g., here, and I think it is worthwhile to take a look at this. One response to these words of caution was that margin debt as a percentage of stock market capitalization is within a normal range. For myself, I want to put this in context. Here is some data. Note how the drop in margin debt and SPX in both 1987 and 1998 barely register. I wasn’t in the business for 87, but I can assure that the LTCM selloff in 1998 was significant in many ways.

There is a pretty nice correlation of peaks (yes, that’s the technical term) between margin debt highs and SPX highs, followed by steep drop-offs. The conclusion is clear: get short when margin debt peaks. Which leads to the equally clear problem: one can’t tell the peak until afterwards. At least for this data, we can feel comfortable about correlation meeting causation. Leveraged buyers are weak hands because their choice is limited by the margin clerk. Once prices start falling, margin selling leads to further margin selling. To address some concerns about how much margin debt is too much, I’ve created two additional charts that re-slice the numbers a bit.

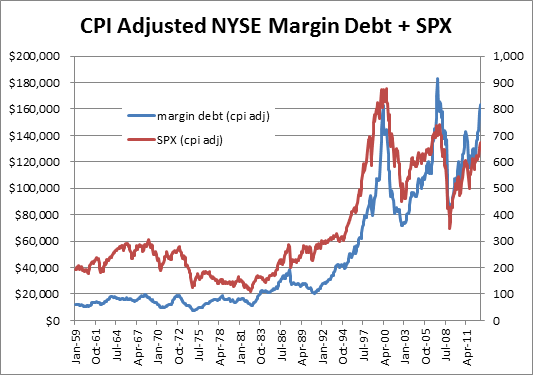

I think that the CPI adjusted margin debt adds some information as it shows that “real” margin debt is about the same as in 2000 rather than being much higher. On the other hand, looking at debt as a percentage of total market capitalization dilutes the information. It shows how the market has become more debt driven than in decades past, but it doesn’t add a red signal at any point. No danger zone for ’87, ’98, ’00, ‘07/08.

What is my conclusion here? Be afraid. Be very afraid. But these things tend to take longer to play out than one expects. In fact, the Rudiger Dornbusch quote from above captures it perfectly. Trades like this get called the widowmaker for a reason. There is evidence of weak hands playing a dangerous game. It would be great if we could find a crowded trade in overpriced assets. Yeah, and then cheap, asymmetric bets to make.

There is more to this story, but it will have to wait for the next post.

[…] Margin debt. Discussed here, note that the most recent release which was subsequent to that post, showed margin debt climbing […]