“Random chance seems to have operated in our favor” — Spock

“In plain, non-Vulcan English, we’ve been lucky” — McCoy

“I believe I said that, Doctor” — Spock

The data shows that there have been large inflows of cash to yield bearing equity strategies. That is not enough to get worried. What I’d like to see before shorting is 1) elevated prices & valuations, 2) an illusion of safety, 3) feedback loops, 4) diminishing ability to put cash to work and 5) a catalyst. Fortunately, we are able to see all of these things in this yield trade.

Valuation: danger ahead for REITs

I first look at the data for non-REIT companies. Above is a chart showing price-to-earnings (P/E) and price-to-book (P/B) data for 4 heavily weighted dividend sectors. Those sectors are: utilities, consumer discretionary, consumer staples and industrials. These are GICS sectors and the data is from Bloomberg. The utilities P/B ratio is quite high. Bluntly, P/E ratios look relatively normal. However, take a look at the next graph showing revenue, earnings per share (EPS) and debt per share. Note:

1) consumer discretionary revenues have not caught up to pre-2008 highs, but EPS is significantly higher

2) revenue and EPS are higher for consumer staples, but debt/share is growing and is double pre-2000 levels

3) despite languishing revenue and EPS, utilities debt/share are at all-time highs

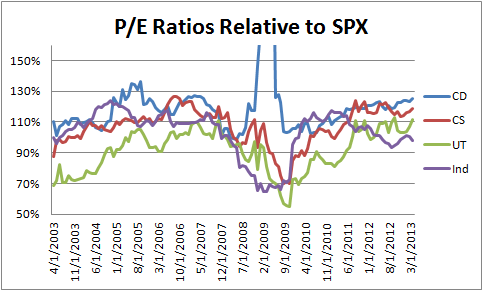

I’ve included another graph showing P/E ratios relative to the SPX P/E. Other than industrials, all of these four sectors look, at least, slightly rich. Utilities, in particular, looks very expensive compared to alternatives in the market. Overall, it looks clear that investors are overpaying for sectors considered to be dividend payers though not necessarily at nosebleed prices. Utilities valuations and debt burdens are showing definite warnings signs and should be avoided, or used as a candidate for the short side of sector pair trading.

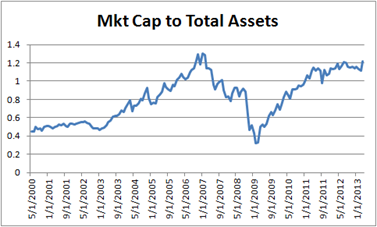

REITs are a different story. I’ve kept them separate because they use a different profitability metric, P/FFO. The data for this article is from Bloomberg and I was unable to get historical FFO data for the S&P REIT Index directly. Instead I took 5 major REITs (BXP, AVB, SPG, KIM, VNO) and aggregated the data. I took simple averages of their P/FFO ratios; not all series went back to 2003 but the latest started 2005. As can be easily seen, on both absolute and relative bases, REITs are at their highest profitability ratios in the last 10 years including during the real estate bubble.

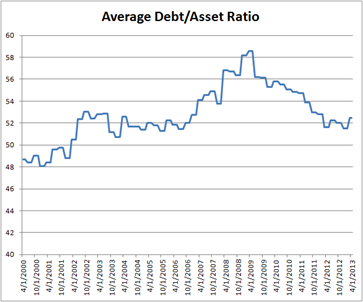

On the surface, it seems as though REITs have cleaned up their debt act a bit since 07/08. However, the reason for the peak of the debt/asset ratio in 2009 was due to the precipitous decline in the value of assets. Now with assets stabilized and even increasing, REITs have increased their debts so that the ratio is back to pre-crisis highs. In addition, the market is giving them an extremely generous market valuation for those assets. Market capitalization, for at least those major 5 REITs, is right back to pre-crisis, i.e., bubble level, highs. REITs are squarely in the danger zone based on valuation.

Illusion of Safety

With the exception of high yield bonds and, possibly, MLPs, dividend and low volatility strategies are touted as being safe (for example, here or here). But the safety that is being offered is measured using the rear-view mirror. Safety is being judged based on past performance – which we know is not a guarantee of future results. Measuring risk based on historical asset movements has three major flaws. The first is that it is measuring movement, not risk. For example, standard deviation does not differentiate between assets bouncing around and an earnings release that qualitatively changes a company outlook. Second, it does not account for asymmetric risk. Option positions are one type of asymmetric risk; buying an asset very cheaply or paying too high a price is another. Third, it creates feedback loops when large amounts of money move based on the same criteria. Low volatility invites larger asset purchases, particularly with leverage. This decreases realized volatility as prices move up which again invites larger purchases. Once inflows inevitably stop, volatility increases, causing risk reduction or margin calls as exposures must be managed based on newly assessed risk outlooks.

Low-volatility investing works by measuring prior period asset movement, much as Value-at-Risk (VaR) does. SPLV, the largest low volatility ETF, bases its holdings on realized volatility over the prior 12 months and rebalances quarterly. The nice thing about low volatility asset management is that it is based on solid empirical data. That’s good except for the part about how the data that was used for the studies did not count on large amounts of money following the same strategy. SPLV does not count on anything else other than qualifying as the 100 stocks out of the SPX with the lowest realized volatility. These assets tend to look like traditional dividend players – and heavy on REITs (10% for SPLV, less for others). If these holdings begin to get volatile, they will be forced to evict them from the portfolio which will then contribute to greater volatility.

Feedback Loops & Diminishing Ability to Buy More

In addition to the volatility based feedback discussed in the section above, there are other feedback loops at play:

1) Margin debt. Discussed here, note that the most recent release which was subsequent to that post, showed margin debt climbing to an all-time high.

2) High levels of bond funds holding equities. Discussed here.

3) Risk parity and similar strategies. Discussed in part 1.

4) Abenomics leads to Yen devaluation and Japanese “exporting” deflation. here and here. With Yen depreciation at least temporarily slowed, expect Japanese money to REITs to slow or stop.

5) One of the most interesting feedback loops also comes from Japan, where they, too are searching for high yield. In the Heard on the Street column from April 15, 2013, it was reported that Japanese investors have been searching for yield in vehicles that invest in US REITs. The key part is that they pay out unrealized (not a typo, unrealized) capital gains on the way up as dividends. That is amazing. One can only imagine the debacle if US REITs stop climbing. Oh yeah, and they are large holders of these stocks, too. According to the article, they own 8.6% of SPG and 10.1% of VNO. For those of you that remember chemistry class, this reminds me of a super-saturated, barely stable solution ready to blow (think Diet Coke & Mentos).

Catalyst

This is the toughest part about investing. Even if one presumes enough to believe that one has the correct analysis, it is no good to be too early (e.g., Abnormal Returns from 2011). What might be a catalyst could turn out to be a bump in the road. That said, I believe that we have seen the catalysts to shake things up. First, FX market volatility has picked up. After hitting multi-year lows at the end of 2012, the JP Morgan global FX volatility index has rebounded to 2010-2011 levels. This is due to Yen weakening. Second, that volatility has spilled over into commodity markets, most noticeably gold & silver. I consider this to be a canary in the coal mine. Finally, the potential for the Fed to slow or stop purchases in the mortgage markets will have a huge impact on volatility and asset prices. Fixed income prices have begun to re-price the possibility of this and it has sent 10 year note yields to their highest level since beginning of 2012 in just a few sessions. Recall too that the Fed effectively sells volatility by buying mortgage paper (there is an embedded pre-payment option).

Conclusion

All well and good, but what is the elevator speech? Too much money, most seemingly leveraged money, is chasing the latest investment craze – yield in dividend stocks. The most distended market is for REITs which looks particularly expensive by benchmark measures. Further, the investor class in REITs is a large set of “weak hands.” That is, they are investors who will need to exit (due to margin calls or structural investment guidelines) at the first sign of trouble and they are too large a proportion of owners to make the exit orderly. While other areas of dividend investing may look rich, REITs are where the focus should be for short ideas. The time is soon approaching when this will occur – already some volatility has been creeping into REIT shares and ETFs. It is hard to imagine that continued inflows will recur. And once the support for an overvalued asset stops, the decline can begin.